House prices, especially in Auckland, are extremely high relative to incomes, but this doesn't mean there is imminent or necessarily large downside risk for house prices.

It is also questionable whether the falls in median house prices reported by REINZ in recent months accurately reflect underlying price behaviour.

When I look at interest costs faced by new buyers in Auckland and nationally as percentages of incomes, there is no housing affordability problem.

Low interest rates have made housing as affordable for new buyers in Auckland as has been the case on average since 1992, while in the rest of the country housing costs, in terms of interest outlays as a percentage of incomes for new buyers, are below average.

High house prices relative to incomes don't in themselves pose a threat as long as interest rates remain low.

The consensus view is that interest rates will head lower this year and remain quite low. Unfortunately, the consensus view is more often wrong than right.

The Raving highlights this in the context of the consensus view on inflation prospects versus my view. What happens to interest rates will ultimately be of most importance to house price behaviour, with what happens to migration of secondary importance, as covered in our pay-to-view housing reports. But this is in the context of the current starting point being one in which the national demand-supply balance in the housing market is still strong and likely to strengthen as buying by foreign investors recovers.

A surprise this year and beyond should be that house price inflation remains more resilient than the Reserve Bank expects, even when Governor Wheeler is eventually forced to hike the OCR.

Low interest costs largely justify high house prices relative to incomes

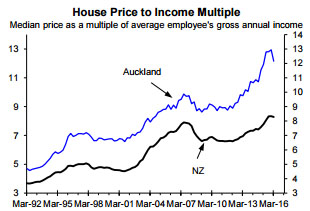

People predicting large falls in house prices because prices are high relative to incomes overlook the massive impact low interest rates have had on housing affordability. The left chart shows median dwelling prices reported by REINZ as multiplies of median individual gross incomes for New Zealand and Auckland. The national and Auckland price/income ratios are well above the levels that existed in 2007 before the last sizeable fall in prices. In August 2007 I wrote the Housing Hell Raving that warned about downside risk to house prices. But do high house prices relative to incomes mean a large fall in house prices is inevitable, especially in Auckland?

It is a very different story when we look at interest costs for new buyers relative to incomes (right chart). The right chart assumes an individual with the median income buys a median-priced house using 80% debt and paying the average current interest rate, with the interest cost expressed as a % of income. Nationally, interest costs relative to incomes for new buyers are a bit below the average since 1992; while even in Auckland the interest cost as a % of income is close to the average level and dramatically below the peak level in 2007.

From the perspective of interest costs, there isn't a housing affordability problem for new buyers, even in Auckland. However, this doesn't take into account that buyers need to come up with much larger deposits relative to incomes than used to be the case, while principal repayments will be larger, putting some pressure on cashflows, especially in Auckland. Low interest rates largely justify high house prices relative to incomes for new buyers, while existing house owners have experienced large increases in wealth as well as having low interest costs. What will happen to interest rates is critical (see below).

The irony is that at the same time as solving the housing affordability problem, low interest rates have played a key part in driving house prices higher and making the underlying housing affordability problem worse (i.e. rising house prices relative to incomes). As an aside, I am wary of the recent falls in median house prices reported by REINZ and the related falls in house prices relative to incomes reported in the left chart above.

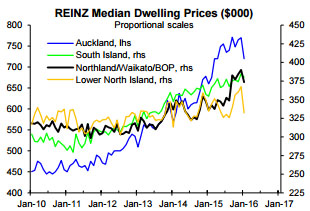

The sharp fall in the median dwelling price reported by REINZ for Auckland would seem to fit with the fall in Auckland dwelling sales following the October tax changes and the November increase in deposit requirements for Auckland investors. However, the reported median dwelling price for the lower North Island, where sales haven’t fallen much, has fallen proportionally more than the Auckland price (adjacent chart). The chart shows significant random variation - spikes and tumbles - in the reported median dwelling prices for all four areas, but especially for the lower North Island. Certainly, the fall in the Auckland median price seems a bit more than can be explained by random variation due to changes in the composition of sales (i.e. a smaller proportion of higher-priced properties selling and a higher proportion of lower-priced ones selling). The tax changes have temporarily at least removed many of the buyers paying premium prices, especially at auctions, but there are suggestions a number of these buyers will return. It is possible quite a bit of the reported fall in the Auckland median price reflects variation in the composition of sales rather than underlying downside in prices, while the lower reported median prices for the other three areas may entirely reflect random variation in the reported median prices rather than underlying downside.

In the Housing Prospects reports I show the demand-supply balances in the national and Auckland market, as well as assessing house price prospects for most cities. In the March report I showed that the tax and Auckland LVR changes have dented the case for upside in Auckland house prices, but have far from killed it, while in most of the rest of the country the case for upside in house prices remains strong.

Two very different views on interest rate prospects

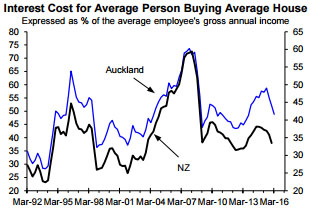

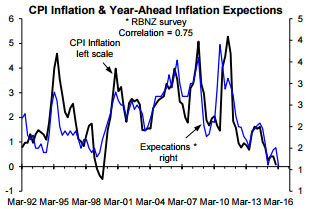

In my assessment of past experiences in NZ and elsewhere, high house prices relative to incomes aren't the threat suggested by some, but rather the risk that at some stage interest rates will be "normalised" (i.e. return to around average levels or maybe even above average at some stage). The adjacent chart updates the top right chart on page 2 but assumes interest rates rebounded to the average level experienced since 1992 (the spikes in the Auckland and national interest costs as a % of income for the average buyer of the average house). If interest rates were at average levels the affordability of Auckland house prices for new buyers would be as challenging as was the case just before the fall in prices in 2008. Nationally the interest cost as a % of income for new buyers wouldn't be as high as the peak in 2007. But when might interest rates increase and is there any risk of a large increase, like the increases in the 1990s and 2000s that eventually culminated in falling house prices in Auckland and most parts of the country? Most bank economists are putting a lot of weight on low CPI inflation and the related fall in inflation expectations (adjacent change). The consensus view is that low inflation expectations are a sign that inflation will be low in the medium-term future Governor Wheeler is supposed to focus on in making OCR decisions, justifying more OCR cuts. This is despite surveys of inflation expectations generally moving up and down with historical inflation, as can be seen in the chart. Current inflation expectations don't tell us anything useful about future CPI inflation. It has been common for periods of higher inflation to follow periods when inflation expectations were low. As is too often the case, the consensus view is based on insufficient consideration of the past experiences. Based on past experience, the bank economists currently calling for more OCR cuts will in the future be calling for OCR hikes when it is revealed that the persistent period of low interest rates has contributed to an inflation problem.

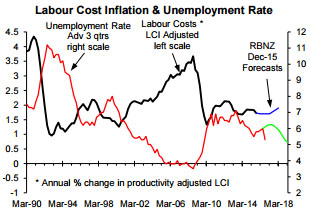

While a rear-view-mirror-based assessment of inflation prospects says the governor should cut the OCR more, a forward-looking approach focused on the core factor relevant to medium-term inflation prospects is starting to politely ring warning bells about inflation rising. The "surprise" fall in the unemployment rate from 6% in the September quarter to 5.3% in the December quarter - red line, left chart below - shouldn't have been such a surprise to the economic forecasters given the rebound in leading indicators of employment growth (e.g. the surge in online job ads reported by the Department of Labour - right chart below). However, the fall in the reported unemployment rate may partly reflect random variation and could be partly reversed this quarter.

The labour market (i.e. wage and salary inflation) is central to medium-term CPI inflation prospects. The left chart below shows the unemployment rate, leading or advanced by three quarters, as a useful leading indicator of the productivity-adjusted measure of labour cost inflation the Reserve Bank (RB) focuses on, as well as the RB's forecasts for both. As covered in our monthly economic reports, there are good reasons for expecting employment growth to be stronger than predicted by the RB and the bank economists, so even if the reported fall in the unemployment rate in the December quarter partly reflects random variation, a key theme going forward should be an earlier and larger fall in the unemployment rate than predicted by the RB (green line, left chart), which will imply earlier and more upside in labour cost inflation.

The RB and the bank economists were blind to the labour cost inflation problem that developed in the mid- 2000s when Governor Bollard made the mistake of allowing the unemployment rate to fall well below the level consistent with keeping inflation at around 2% on average over the medium-term. They are just as blind now to the risk that the labour market will be allowed to tighten excessively.

In the mid-2000s I was a lone voice warning about the upside risk to interest rates, with history repeating itself on this front, although the upside risk this time around isn't as large as was the case in the 2000s, as outlined in our monthly economic reports.

With interest rates so critical to housing affordability, having quality insights into interest rate prospects and the implications for the demand-supply balance in the house market is critical if you want a forewarning of when the current boom in house prices will end, when downside risk to house prices will emerge and whether there will be the risk of a sizeable fall in house prices. These insights are contained in the Housing Prospects reports, while our monthly economic reports provide more detailed insights into what the RB and bank economists are overlooking. Prospects for economic growth, employment growth, consumer spending growth and interest rates are currently very different from the consensus view, which is nothing new given the poor forecasting track record the RB and bank economists have (e.g. use the following link to a related Raving - http://sra.co.nz/pdf/TradeSecrets.pdf).

*Rodney Dickens is the managing director and chief research officer of Strategic Risk Analysis Limited.