NZ is doomed to experiencing major housing cycles in part because of the link between interest rates and migration and the tendency for the Reserve Bank to conduct misguided monetary policy experiments (i.e. cut interest rates excessively when there is already an upturn in immigration/net migration boosting the economy and housing market).

This Raving focuses on the link between interest rates and immigration.

The housing market is in the latter stages of benefiting from the combination of low interest rates and high immigration/net migration, with the resulting housing boom fuelled further by increased activity by investors albeit that this has been temporarily set back by the latest lending restrictions.

It is inevitable that the latest boom like all past booms will be followed by a major downturn in the housing market, including for residential building.

This is in part because in time interest rates will need to be increased to the extent it generates a hard landing for the economy, meaning much lower employment growth and reduced demand for immigrant workers. From currently still being positive factors for the housing market, the two main cyclical drivers will end up turning against it and in turn drive reduced activity by investors.

Why does NZ experience such major housing cycles?

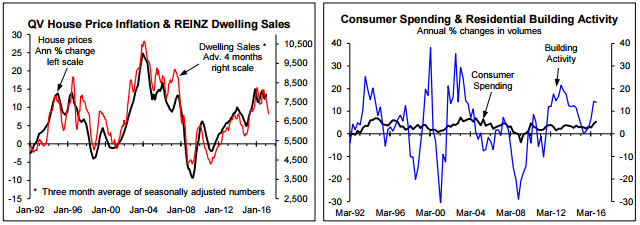

As is the case in many countries, it is normal for NZ to experience major housing cycles roughly once a decade. This is shown in the left chart for the number of existing dwelling sales and house price inflation and in the right chart for annual growth in residential building activity that is dramatically more cyclical than annual growth in consumer spending. The massive cycles create a nightmare for people managing firms impacted by the housing and residential building cycles.

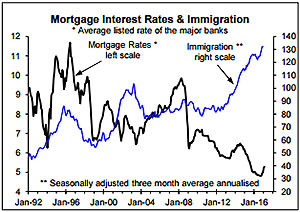

Interest rates and immigration are the major drivers of cycles in the existing housing market while interest rates and net external migration (i.e. immigration less emigration) are the major drivers of cycles on residential building. The adjacent chart shows that both interest rates and immigration experience major cycles but one of the key issues is that there is a consistent tendency for upturns in immigration (and in net migration) to roughly coincide with periods of falling/low interest rates as can be seen in the adjacent chart. The combination of falling interest rates and rising immigration/net migration are the key drivers of the major housing upturns experienced in the past but it is also normal for this to be followed by periods of higher interest rates and falling immigration/net migration. In addition, periods of low/falling interest rates and high immigration/net migration fuel increased buying/building by investors, just as periods of sustained high interest rates and lower immigration/net migration end up choking off buying/building by investors.

Interest rates and immigration are the major drivers of cycles in the existing housing market while interest rates and net external migration (i.e. immigration less emigration) are the major drivers of cycles on residential building. The adjacent chart shows that both interest rates and immigration experience major cycles but one of the key issues is that there is a consistent tendency for upturns in immigration (and in net migration) to roughly coincide with periods of falling/low interest rates as can be seen in the adjacent chart. The combination of falling interest rates and rising immigration/net migration are the key drivers of the major housing upturns experienced in the past but it is also normal for this to be followed by periods of higher interest rates and falling immigration/net migration. In addition, periods of low/falling interest rates and high immigration/net migration fuel increased buying/building by investors, just as periods of sustained high interest rates and lower immigration/net migration end up choking off buying/building by investors.

There are some major flaws in how monetary policy is conducted in NZ (and globally), with one being the tendency of the Reserve Bank to cut the OCR excessively during times of rising immigration and net migration. It is inevitable that significant interest rate cuts when combined with a large increase in immigration/net migration will drive housing booms including fuelling investor activity. But there is more to it than this because of the link between interest rates and immigration.

There are some major flaws in how monetary policy is conducted in NZ (and globally), with one being the tendency of the Reserve Bank to cut the OCR excessively during times of rising immigration and net migration. It is inevitable that significant interest rate cuts when combined with a large increase in immigration/net migration will drive housing booms including fuelling investor activity. But there is more to it than this because of the link between interest rates and immigration.

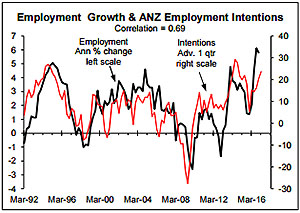

The result of cutting the OCR excessively at the time of a major upturn in immigration/net migration is overly strong GDP and employment growth which is visible in the case of employment growth in the adjacent chart in the mid-1990s, mid-2000s and again recently. The strong employment growth then plays a part in boosting immigration.

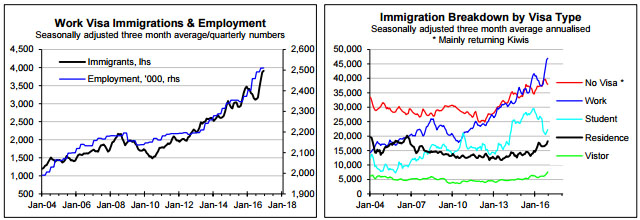

The left chart below shows a quite close link between employment numbers and the numbers of immigrants arriving with work visas. The right chart shows the growing percentage of total immigrants made up by immigrants arriving with work visas. A strong local labour market also plays a part in encouraging more Kiwis to return from OE as measured by no visa immigrants shown right chart below (red line) although what is happening in the Australian labour market is a more significant driver of the number of Kiwis returning from OE and the number of Kiwis emigrating from New Zealand.

There are a number of important dynamics that drive migration cycles as covered in our monthly housing and residential building reports including developments in the Australian labour market. But one of the reasons why housing cycles are so extreme is a link between interest rates and immigration/net migration cycles. When the Reserve Bank makes the mistake of overly stimulating the economy with OCR cuts at the time there is already an upturn in immigration/net migration it adds to the upturn in immigration.

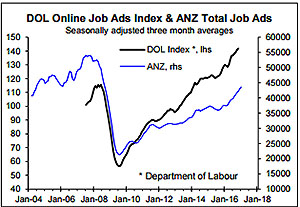

The massive cyclicality in job ads shown in the adjacent chart is partly the result of the mistakes the Reserve Bank seems to repeatedly make of cutting interest rates excessively when economic growth is already being stimulated by a major upturn in immigration/net migration. But then having driven an overly tight labour market the Reserve Bank ends up needing to manoeuvre a hard landing for the economy and labour market to restore more balanced bargaining power between employers and employees which drives a major housing downturn.

The massive cyclicality in job ads shown in the adjacent chart is partly the result of the mistakes the Reserve Bank seems to repeatedly make of cutting interest rates excessively when economic growth is already being stimulated by a major upturn in immigration/net migration. But then having driven an overly tight labour market the Reserve Bank ends up needing to manoeuvre a hard landing for the economy and labour market to restore more balanced bargaining power between employers and employees which drives a major housing downturn.

Job ads have surged significantly in the last year which means more employers will be looking to attract staff from overseas which will be the main factor behind the upturn in immigrants arriving with work visas although this may partly reflect random variation or people getting in ahead of recent tightening in immigration criteria by the government (blue line top right chart). Critically, major upturns in immigration fuel demand in the economy and labour market more than they boost the supply of labour especially when they are combined with falling interest rates. This is contrary to what seems to be a reasonably widely held view that immigration boosts labour supply more than it boosts labour demand. Immigrants need to restock a wide range of durable goods which is why they add more to demand than supply in the economy especially in their first year in the country.

NZ is currently in the latter stages of the latest major housing upturn driven by the combination of low interest rates and high immigration/net migration; with these in turn driving increased activity by investors albeit for the moment that has been at least temporarily set back by the latest lending restrictions. However, just as the combination of interest rate cuts and high immigration/net migration have driven the latest housing boom it is inevitable that the latest misguided monetary policy experiment ultimately results in the need for a hard landing that will mean much slower employment growth and reduced demand for immigrant workers by employers; and that this results in reduced activity by investors. It is inevitable that there will be another major housing downturn and via our existing housing market and residential building reports we will probably again be the only forecasters that provide a timely advance warning.

*Rodney Dickens is the managing director and chief research officer of Strategic Risk Analysis Limited.