Two of the main factors used to justify the five OCR cuts Governor Wheeler has delivered over the last year will not have the impact on the economy assumed by the Reserve Bank and the economic forecasters in general.

Specifically, the negative impact of the fall in dairy farm incomes on economic growth is greatly overstated as is the relevance of the fall in expectations of future inflation.

The housing market has for some time been telling us that interest rates are too low while the labour market is starting to quietly ring the warning bell about future inflation risks.

With much of the boost from the OCR cuts still in the pipeline the labour market will head more into inflation risk territory before the governor realises his mistake.

The misguided OCR cuts pose a range of opportunities and threats.

When the main justifications for OCR cuts are flawed it is time to get informed

Since June 2015 Governor Wheeler has delivered five OCR cuts while some bank economists continue to argue that he should cut at least once more. The large fall in dairy farm incomes was used as a major justification for OCR cuts initially on the basis it would have a significant negative impact on economic growth. Recently the justification for cuts has shifted more to the fall in expectations about future inflation. Low inflation expectations are supposed to mean inflation will remain too low, justifying OCR cuts to boost economic growth and inflation. The problem is both these justifications for OCR cuts are flawed.

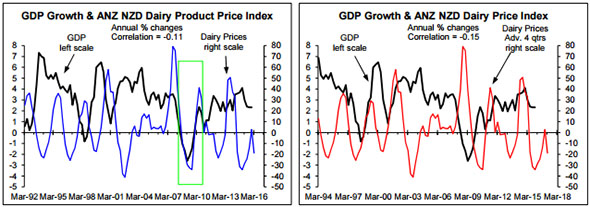

The historical experience says dairy product prices have little impact on economic growth. The left chart shows no clear link between the annual % change in dairy product prices and annual GDP growth. Falls in dairy product prices are more often associated with above average than weak GDP growth. This is the case even if I allow 12 months for changes in dairy product prices to impact on GDP growth (right chart).

Other factors generally swamp the impact of changes in dairy farm incomes on economic growth although in extremely rare situations, like the experience following the emergence of the financial crisis, the other more important drivers can line up with a fall in dairy product prices and cause a recession (see the boxed area in the left chart above). But this is the exception that proves the rule that dairy product prices are of little relevance to economic growth. With only a little over 12,000 dairy farms nationally there aren't enough of them to have a major impact on economic growth even if they cut spending significantly; especially in the current situation in which super-charged net migration is adding around 70,000 people to the population per annum and interest rates are at the lowest level on record.

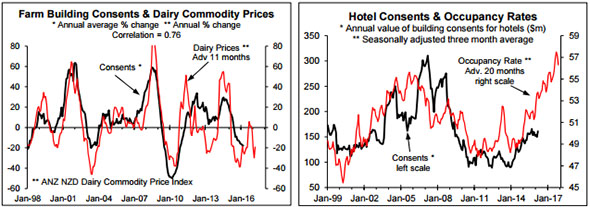

Certainly, the fall in dairy product prices is resulting in a large fall in consents for farm buildings (see the left chart below that shows the annual % change in dairy product prices leading or advanced by 11 months relative to annual growth in the value of consents for farm buildings). But why focus on this when the other contender for NZ's No. 1 export earner - tourism - is booming and the high occupancy rates in commercial accommodation point to further significant upside in consents for hotels, motels and other short-term accommodation after advancing the occupancy rate by 20 months (right chart).

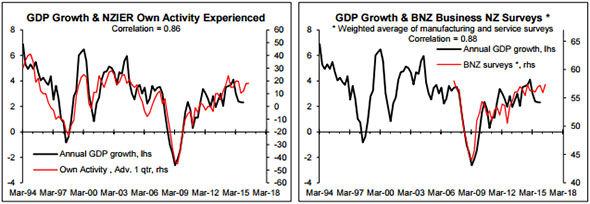

Rather than support the view that economic growth is going to slow more after the recent slowdown or remain low, the most useful leading indicators of near-term economic growth point to it running around 3.5- 4% although they aren't always reliable (two charts below).

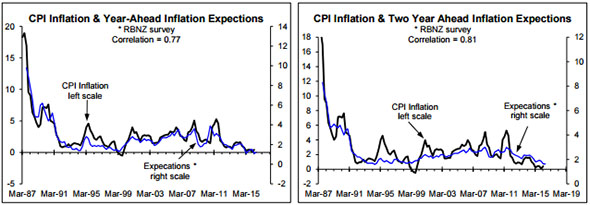

More recently the focus of those calling for OCR cuts has been on the fall in inflation expectations. The left chart below shows the relationship between the Reserve Bank's (RB's) survey of year-ahead inflation expectations and actual CPI inflation and the right chart shows the relationship between the RB's survey of two-year-ahead inflation expectations and actual inflation. Year-ahead expectations go up and down with actual inflation. Periods of low year-ahead inflation expectations have often been quickly followed by rebounds in inflation. The RB's survey of two-year-ahead inflation expectations is less reactive to the shortterm swings in actual inflation than is the one-year-ahead survey, but it still largely moves with actual inflation rather than being predictive of future inflation (right chart below).

Evidence the OCR cuts are unfounded and implications for businesses and investors

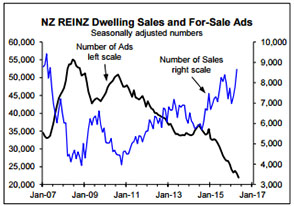

The housing market is the most interest rate sensitive part of the economy and booming house sales is a sure sign interest rates are too low. Having been hurt quite a bit by the October tax changes and Auckland November LVR changes the national number of existing dwelling sales reported by REINZ has rebounded (blue line, adjacent chart). The rebound in sales has eaten further into the stock of property for sale based on the number of for-sale listings on www.realestate.co.nz (black line). The demand-supply balance in the housing market is back to being super-charged, which will be reflected in house price inflation strengthening to well above levels that are healthy.

The housing market is the most interest rate sensitive part of the economy and booming house sales is a sure sign interest rates are too low. Having been hurt quite a bit by the October tax changes and Auckland November LVR changes the national number of existing dwelling sales reported by REINZ has rebounded (blue line, adjacent chart). The rebound in sales has eaten further into the stock of property for sale based on the number of for-sale listings on www.realestate.co.nz (black line). The demand-supply balance in the housing market is back to being super-charged, which will be reflected in house price inflation strengthening to well above levels that are healthy.

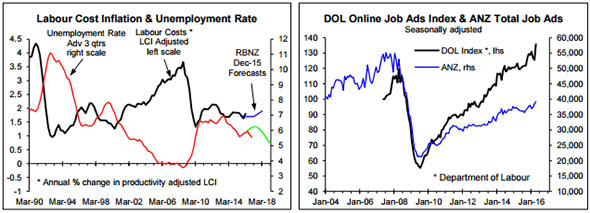

While the housing market provides the first indication if interest rates are too low, the labour market is where the more important inflation implications of excessively stimulatory monetary policy get confirmed. It takes several quarters for excessively stimulatory monetary policy to be reflected in a falling unemployment rate and several more quarters for it to be reflected in upside in the purely inflationary component of labour cost inflation (i.e. the increase in labour costs that isn't justified by productivity growth and will therefore boost unit production costs and encourage producers/employers to put up prices).

The left chart below shows that the unemployment has fallen in the last couple of quarters when a two quarter moving average is used to smooth the volatility in the quarterly numbers (red line). This contrasts with the RB's December prediction that it would increase (green line) and predictions of upside by most of the bank economists (use the following link to the October 2015 Raving that criticised the Westpac economists for predicting a rising unemployment rate). The fall in the unemployment rate is consistent with GDP having grown at a 3.5% annualised rate in the second half of 2015 (i.e. it shouldn't have been a surprise to the RB and other forecasters). While surveys of inflation expectations provide little if any insight into future inflation, the unemployment rate is a pretty accurate leading indicator for productivity-adjusted labour cost inflation. The peak correlation at -0.84 (akin to a 84% mark in an exam) is with the unemployment rate leading by three quarters, with this reflected in the left chart by the unemployment rate line being advanced or shifted to the right by three quarters.

In my assessment of the historical experience, if the unemployment rate falls below around 5.5-5.8% (i.e. around the current level) it will fuel, with around a three quarter lag but at times with a slightly longer lag, higher productivity-adjusted labour cost inflation than consistent with Governor Wheeler's 2% CPI inflation target. If GDP growth continues to run at around the recent rate of 3.5%, in line with what the leading indicators are suggesting, the unemployment rate will continue to fall. The somewhat volatile job ads indicators are suggesting employment growth prospects are strong (right chart above), which is vaguely consistent with what the leading indicators of GDP growth are predicting.

It takes around a year for OCR cuts to fully impact on economic growth and a little longer for them to impact on the unemployment rate. The obvious implications of this is that the fall in the unemployment rate that will occur as a result of the five OCR cuts delivered over the last year still lies ahead. The risk appears to be high that the OCR cuts will fuel higher productivity-adjusted labour cost inflation over the next couple of years allowing for the normal lags in the process. Having not predicted the fall in the unemployment rate, the RB and the economic forecasters are playing down the implications of the fall while some of them are calling for one OCR cut that will only drive it more into inflationary territory.

If I am right in suggesting the OCR cuts were the result of excessive focus on factors that have little if any bearing on the medium-term inflation outlook Governor Wheeler is supposed to focus on, it will have major implications on a range of fronts. This includes house prices, residential building, interest costs, labour costs, consumer spending and the exchange rate. To find out what the implications are for these areas and others I suggest you enquire about our pay-to-view reports if you don't already subscribe to them. In my assessment the outlook on a range of fronts is significantly different to the consensus view meaning we can more than ever provide valuable insights to our clients; insights you won't get from the bank economists or the RB's forecasters.

*Rodney Dickens is the managing director and chief research officer of Strategic Risk Analysis Limited.